When IFRS 16 entered into force on 1 January 2019, it did not simply change an accounting rule. It changed the operational architecture of how organisations manage their lease portfolios. What had previously been a disclosure exercise — listing off-balance-sheet commitments in the notes to the financial statements — became a continuous accounting obligation touching contracts, fixed assets, the general ledger, and financial reporting every single month.

Seven years on, many organisations are still managing this obligation partially manually. Spreadsheets sit alongside SAP. Finance teams recalculate lease liabilities at each period close. Contract modifications trigger email chains rather than system updates. The audit trail is reconstructed rather than generated.

The combination of SAP CLM and SAP RE-FX exists precisely to solve this — and when implemented correctly, it eliminates the manual layer entirely.

What IFRS 16 Actually Requires — And Why It Is Harder Than It Looks

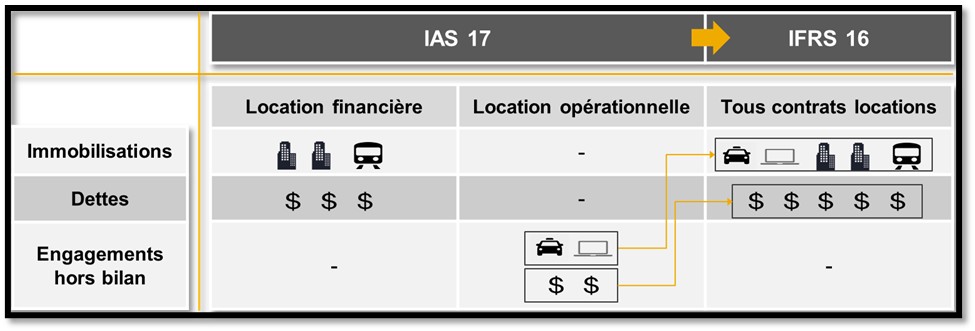

The core requirement of IFRS 16 is straightforward in principle: lessees must recognise a right-of-use asset and a corresponding lease liability on the balance sheet for substantially all lease contracts. The asset represents the right to use the underlying asset over the lease term. The liability represents the present value of future lease payments, discounted at the rate implicit in the lease or the lessee’s incremental borrowing rate.

In practice, the ongoing complexity is significant.

At inception, every qualifying lease requires a calculation of the right-of-use asset value and the lease liability. These calculations depend on the lease term — including the assessment of optional renewal periods that are reasonably certain to be exercised — the lease payment schedule, and the applicable discount rate. None of these inputs are static.

Throughout the life of the contract, the standard requires remeasurement whenever there is a modification to the lease term, a change in the assessment of whether a purchase option will be exercised, a change in the amounts expected to be payable under a residual value guarantee, or a change in the future lease payments resulting from a change in an index or rate. Each remeasurement generates new accounting entries and updates to both the asset and liability carrying values.

At lease end — or in the event of early termination — the asset must be derecognised and any gain or loss on termination must be recognised in the income statement.

For an organisation managing tens or hundreds of lease contracts across multiple jurisdictions, multiple currencies, and multiple contract types, managing this manually is not just operationally burdensome. It is a source of material accounting risk.

SAP RE-FX: The Foundation Your Lease Data Requires

SAP RE-FX — Flexible Real Estate Management — is the prerequisite module for any serious CLM implementation involving property assets. It is the system of record for your real estate portfolio: the properties you occupy, the surfaces you lease, the rent conditions that apply, the indexation schedules that govern annual rent adjustments, and the critical dates — renewal options, break clauses, expiry dates — that determine how each contract should be assessed under IFRS 16.

RE-FX manages the operational reality of a lease portfolio with a level of granularity that general contract management tools cannot match. Individual objects within a property can be managed separately. Rent conditions can include fixed components, variable components, and service charge elements that may or may not qualify for inclusion in the IFRS 16 lease liability calculation. Indexation rules — whether based on a consumer price index, a construction cost index, or a fixed escalation percentage — are managed within the system and applied automatically at the appropriate intervals.

This granularity matters because IFRS 16 requires precision. The lease liability is not simply the total of future rent payments. It is the present value of the payments that are in scope under the standard — which requires careful separation of lease components from service components, and careful assessment of variable payments that depend on an index or rate versus those that are genuinely usage-based and therefore excluded.

RE-FX provides the data foundation that makes this precision possible. Without it, CLM is working from incomplete inputs.

SAP CLM: Where the IFRS 16 Engine Lives

SAP CLM — Contract and Lease Management — is the module that takes the lease data managed in RE-FX and applies the IFRS 16 accounting treatment automatically.

When a lease contract is active in RE-FX, the relevant data flows into CLM: the lease term, the payment schedule, the applicable components, the discount rate. CLM calculates the right-of-use asset and lease liability at inception using the correct present value methodology and creates the opening accounting entries automatically.

From that point forward, CLM manages the ongoing accounting treatment without manual intervention. Each month, it generates the interest expense entry — the unwinding of the discount on the lease liability — and the depreciation entry on the right-of-use asset. Each month, it processes the lease payment and allocates it between the repayment of principal and the interest charge. The entries post directly to SAP FI through the integration between CLM and the general ledger.

When a contract in RE-FX is modified — a rent indexation is applied, a lease extension is agreed, an early termination option is exercised — CLM receives the updated data and performs the remeasurement calculation automatically. The revised lease liability is computed using the updated payment schedule and the current discount rate applicable at the modification date. The right-of-use asset is adjusted accordingly. The remeasurement entries are generated and posted without requiring manual calculation or journal entry preparation.

The FI-AA Integration: Right-of-Use Assets as Fixed Assets

One of the aspects of the CLM architecture that organisations sometimes underestimate is the integration with SAP FI-AA, the fixed asset accounting module.

Under IFRS 16, a right-of-use asset is, functionally, a fixed asset. It has an initial value. It depreciates over its useful life — which in this context is the lease term. It may be subject to impairment. It is derecognised when the lease ends. These are fixed asset accounting events, and the most robust way to manage them in SAP is through FI-AA.

When CLM creates a right-of-use asset, it automatically creates the corresponding asset master record in FI-AA. The depreciation key, the useful life, and the asset value are all transmitted from CLM based on the contract parameters. From that point, FI-AA manages the depreciation run in exactly the same way it manages depreciation for any other fixed asset in the register.

When the contract is modified and CLM performs a remeasurement, FI-AA receives the updated asset value and adjusts the depreciation schedule going forward. When the lease ends, CLM triggers the asset retirement in FI-AA — with automatic recognition of any gain or loss on derecognition.

The result is a fixed asset register that includes all right-of-use assets alongside owned assets, with consistent accounting treatment and a single depreciation run covering the entire asset base.

What Correct Implementation Actually Looks Like

The technical capability of SAP CLM and RE-FX is well-established. The difference between implementations that deliver this capability reliably and those that create ongoing operational problems lies almost entirely in the diagnostic work done before configuration begins.

The most common implementation failure mode is configuring CLM against a lease portfolio that has not been properly audited. Contracts that should be in scope for IFRS 16 are missing from RE-FX. Contracts that are in RE-FX have incomplete or inaccurate data — discount rates that were never updated, renewal options that were not assessed, rent conditions that do not correctly separate lease and service components.

When CLM is configured on top of this foundation, it automates the wrong calculations. The right-of-use assets and lease liabilities it generates do not reflect the true obligations of the organisation. The accounting entries it posts are systematically incorrect. And because the errors are generated automatically at scale, they are harder to detect than the equivalent manual errors would be.

A diagnostic-first approach to CLM implementation begins with a full audit of the existing lease portfolio — identifying every contract that may be in scope, assessing the data quality of the RE-FX records, validating the discount rates and lease term assessments, and reconciling the current carrying values of right-of-use assets and lease liabilities against an independent recalculation.

This audit typically takes three to four weeks. It almost always identifies corrections that need to be made before CLM configuration begins. And it ensures that when the system goes live, the outputs it generates are trusted — by the finance team, by internal audit, and by external auditors.